Closing

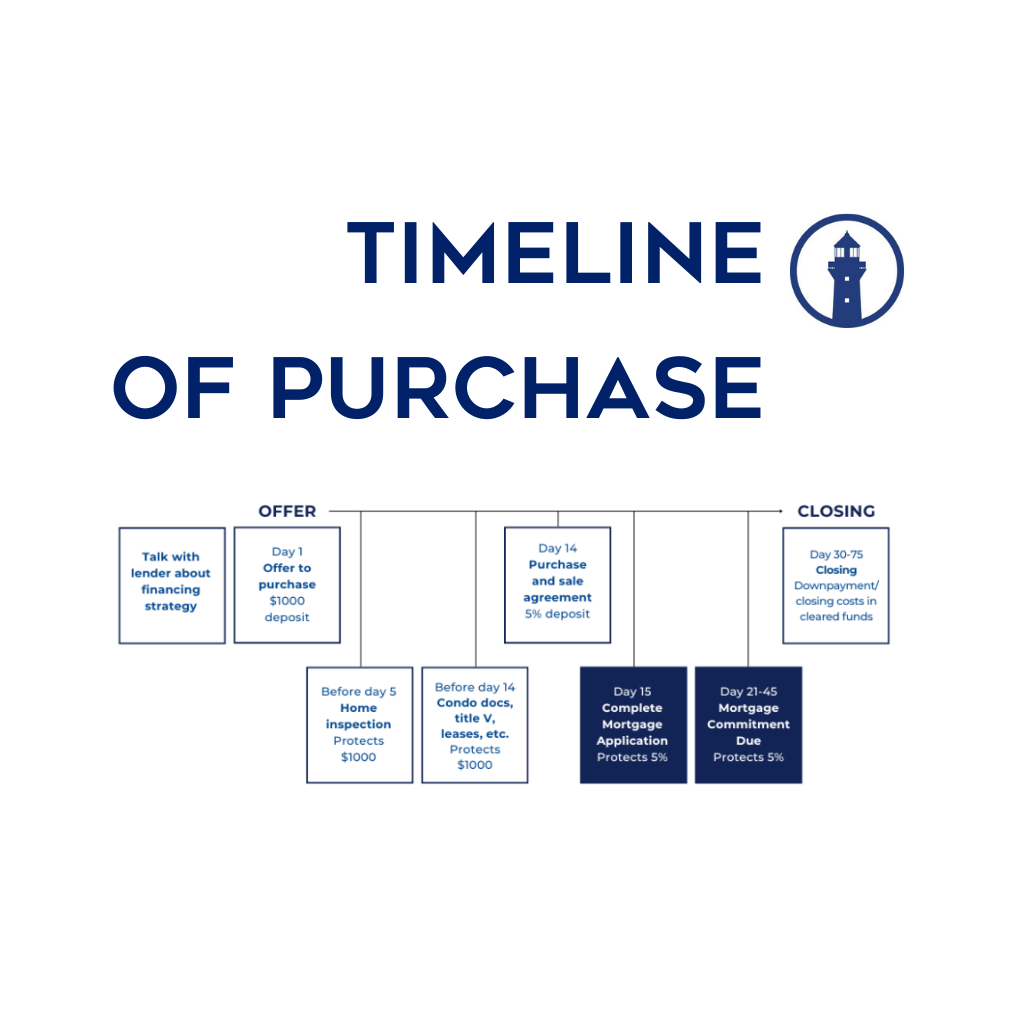

Once your loan is approved and closing is just a few days away, there are several important steps to finalize. You will need to prepare

We use third-party cookies that help us analyze how you use this website, store your preferences, and provide the content and advertisements that are relevant to you. However, you can opt out of these cookies by checking "Opt Out" and clicking the "Save My Preferences" button. Once you opt out, you can opt in again at any time by unchecking "Opt Out" and clicking the "Save My Preferences" button.

Once your loan is approved and closing is just a few days away, there are several important steps to finalize. You will need to prepare

The mortgage contingency is a crucial component of the home-buying process. It outlines your commitment to securing financing for the property purchase. Specifically, you notify

Upon completing (or waiving) your due diligence, the next step is to sign a Purchase and Sale Agreement (P&S). This step is somewhat unique to