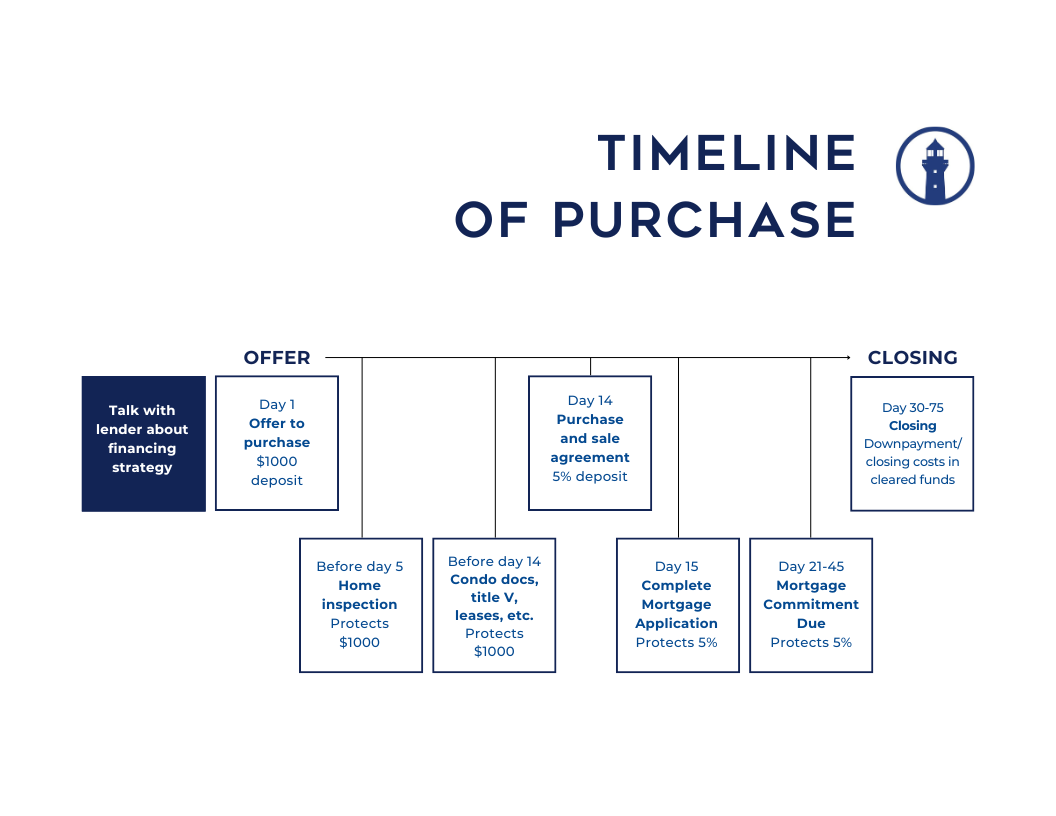

Your financing strategy

We encourage our clients to consult with a lender about their financing strategy. This includes discussing plans with their financial advisor or identifying the sources of their funds, whether they come from a work agreement, family support, or other means, and to address these aspects upfront.

Clients often interpret this as a need for a pre-approval letter before looking at houses, but that is not our primary focus. What we seek to understand and encourage our clients to know is the type of loan they will pursue and where their sources of capital will originate. These factors significantly impact the kind of property they will buy.

It’s not just about the purchase price; it’s about understanding the varying down payment requirements for different properties, and whether certain types of properties can be financed with the chosen loan. The decision involves more variables than simply having a set amount of money or choosing a monthly expenditure. We advise clients to speak with a knowledgeable lender early in the process to comprehend how these different choices will influence the finances of the transaction and their overall decisions.

We meticulously examine the financial aspects of these scenarios to identify what makes the most sense over various timelines, such as a 3-5 year period or a 10-15 year period. Our goal is to ensure that the decision aligns with their long-term goals and needs. We are committed to walking clients through this process to ensure they are making the right choice at the right time.

Several aspects of a condominium complex can impact the types of mortgages available to you. One key factor is the owner occupancy rate of the complex. A lower owner occupancy rate can limit the variety of loans you can obtain, potentially requiring a much higher down payment or even necessitating a cash purchase instead of securing a mortgage. Additionally, condo fees, which cover expenses like maintenance, snow removal, and building repairs, should be factored into your overall financial planning. While these fees may seem high, they can mitigate the risk of unexpected large expenses, offering a more predictable financial commitment.

Many individuals believe that single-family homes are more affordable due to the absence of condo fees. However, it’s important to evaluate the total costs associated with homeownership. For a single-family home, you might face significant expenses such as a new roof, heating system, or general maintenance, which can cost tens of thousands of dollars. Additionally, single-family homeowners are responsible for consistent expenses like water bills, snow removal, and other maintenance tasks. While these costs are not monthly fees like condo fees, they can add up significantly over time and lead to large, unexpected expenses.

When examining multi-family homes, such as two-family or three-family properties, it’s crucial to understand the differences in available financing compared to single-family homes. For example, while you might target a $1 million single-family home due to a comfortable down payment and loan rate, you could find a similar or even better financial situation by opting for a two-family property priced at $1.2 million or $1.3 million. This is because you can often secure a larger loan for multi-family properties without altering your interest rate or down payment requirements. Additionally, owning a multi-family property can provide rental income, offsetting some of your mortgage costs and potentially improving your overall financial situation.

The Purchase and Sale (P&S) process in Massachusetts is relatively unique and not commonly practiced in other regions. A notable aspect is the substantial deposit required, which can catch many buyers off guard due to the quick progression of events. We advise clients to have their P&S deposit funds readily available in cash or a near-cash equivalent before making an offer.

It’s crucial to discuss the source of these funds with your lender upfront and ensure the funds remain in the designated account without being moved. Any movement of funds will necessitate a detailed paper trail, which can complicate and delay the approval process. Therefore, to streamline the process and avoid unnecessary complications, place the funds where your lender directs and refrain from moving them.