Mortgage contingency

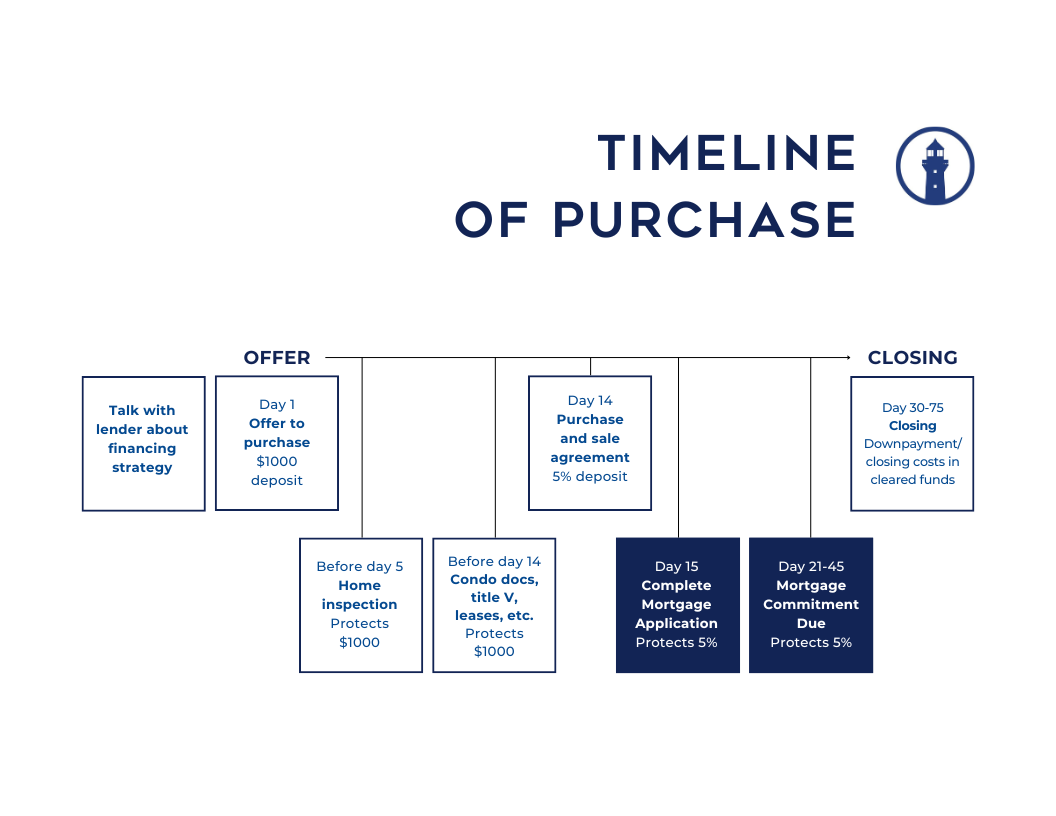

The mortgage contingency is a crucial component of the home-buying process. It outlines your commitment to securing financing for the property purchase. Specifically, you notify the seller that you are applying for a loan, specifying the down payment amount and the date by which you will secure loan approval. This commitment is made when you sign the Purchase and Sale agreement.

Important reminder: To ensure the protection of your deposit, you must apply for the loan as agreed and complete the application around the time you sign your Purchase and Sale. If you opt for a different loan with a smaller down payment or fail to finalize the loan application within the stipulated timeframe, you risk losing the protection offered by the mortgage contingency. It is crucial to avoid changing your mortgage or shopping for new rates at this point forward.

Maintain liquidity: Ensure that the rest of your funds required for the purchase are readily accessible. Avoid making significant purchases, opening new lines of credit, or changing jobs during this critical phase.

Await the commitment letter: Once your mortgage application is approved, you’ll receive a commitment letter from the bank outlining the terms and conditions of the loan. Stay in close communication with your lender and promptly provide any additional documentation they may require.

Confidentiality of commitment letter: The commitment letter contains sensitive financial information and should be treated with utmost confidentiality. Share this information only with your buyer team, including your attorney and real estate agent.

When purchasing a property, a title search is a fundamental step conducted by your attorney and the bank. The purpose is to unearth any existing claims or liens against the property’s title. These could include unpaid taxes, mortgages, or legal disputes that might cloud the ownership rights. By conducting a thorough title search, buyers can ensure they’re acquiring a clear and marketable title, free from encumbrances.

While a title search minimizes the risks associated with property ownership, securing title insurance provides an added layer of protection. Title insurance protects buyers and lenders against any unforeseen issues that might arise after the purchase is complete. This policy offers financial coverage for legal expenses or losses incurred due to undiscovered defects in the title.

In addition to title insurance, securing homeowner’s insurance is essential for safeguarding your investment. Homeowner’s insurance offers financial protection against damages caused by unforeseen events such as fire, theft, or natural disasters. Lenders typically require buyers to obtain homeowner’s insurance before finalizing the mortgage loan.